Loan Management Systems are digital frameworks designed to handle the lifecycle of a loan, from application to repayment.

Over time, traditional paperwork-heavy lending processes have evolved into structured digital systems that help institutions and individuals manage loans more efficiently. Terms such as loan management system, loan management software, and lending management system are often used to describe platforms that centralize loan data, automate workflows, and track repayments.

These systems typically combine multiple functions. A loan origination software component manages the initial application and approval stages, while loan servicing software handles repayment tracking, interest calculations, and account updates. In recent years, digital loan platform solutions have become more common, allowing borrowers and lenders to interact through web or mobile interfaces.

For beginners, these systems may appear complex, but at their core, they aim to simplify how loans are processed and monitored. For professionals, they provide structured tools to manage large volumes of loan accounts with consistency and accuracy.

Importance

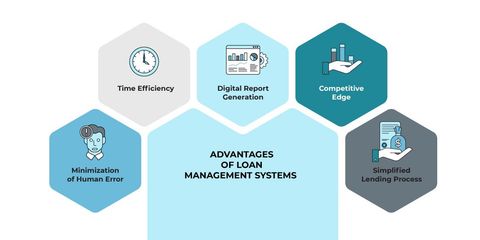

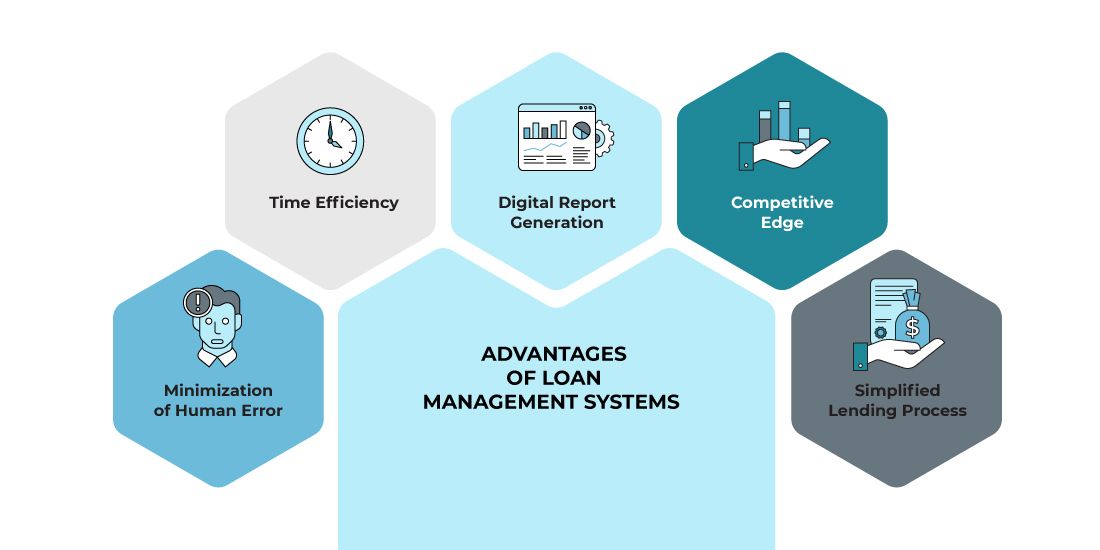

Loan Management Systems play a significant role in modern financial ecosystems. They are used by banks, non-banking financial companies, credit institutions, and even small lending groups to manage lending activities.

One key reason these systems matter is efficiency. Manual processes often lead to delays, calculation errors, and incomplete records. A loan processing software solution reduces these issues by automating tasks such as document verification, interest computation, and repayment schedules.

Another important factor is transparency. Borrowers can track their loan status, EMI schedules, and outstanding balances using loan tracking software or EMI management software. This clarity helps individuals plan their finances better.

From a broader perspective, these systems also support:

- Financial inclusion, where digital loan platforms make lending accessible in remote areas

- Risk management, where credit management systems evaluate borrower profiles

- Compliance, where records are maintained in line with regulatory requirements

For professionals, especially those handling multiple loan accounts, lending software solutions provide structured workflows that reduce administrative burden and improve record accuracy.

Recent Updates

Recent developments in loan management systems reflect a shift toward automation, integration, and data-driven decision-making. Many modern loan automation software platforms now include artificial intelligence features that assist in credit scoring and fraud detection.

Cloud-based systems have become more common, allowing institutions to access loan data from different locations without relying on local infrastructure. This has also improved collaboration between teams handling loan origination, approval, and servicing.

Another noticeable trend is the integration of digital loan platforms with payment systems. Borrowers can now make repayments through mobile apps, and the system automatically updates their loan records in real time.

There has also been increased focus on user experience. Interfaces are being designed to be more intuitive so that even non-technical users can navigate loan management software easily.

Additionally, regulatory reporting tools are being embedded within systems, helping organizations generate reports required by authorities without manual compilation.

Laws or Policies

Loan Management Systems operate within a framework of financial regulations that vary by country. In India, lending activities are governed by institutions such as the Reserve Bank of India. These regulations influence how loan data is collected, stored, and processed.

Key policy areas include:

- Data protection rules, which ensure that borrower information is securely stored and handled

- KYC (Know Your Customer) requirements, which verify borrower identity before loan approval

- Fair lending practices, which prevent discrimination and ensure transparency in loan terms

- Reporting standards, which require institutions to maintain accurate loan records

Loan management software often includes built-in compliance features to align with these policies. For example, loan origination software may include identity verification steps, while loan servicing software maintains repayment histories for auditing purposes.

Digital lending guidelines have also evolved, especially with the growth of online lending platforms. These guidelines emphasize transparency in interest calculations, clear communication of terms, and proper grievance handling mechanisms.

Tools and Resources

Various tools and resources support the effective use of loan management systems. These tools are used by both individuals and organizations to manage loans and understand financial commitments.

Common resources include:

- EMI calculators, which help estimate monthly repayments based on loan amount, tenure, and interest rate

- Loan tracking software dashboards, which display payment history and outstanding balances

- Credit management systems, which assess borrower creditworthiness using financial data

- Loan automation software, which reduces manual intervention in approval and processing workflows

Below is a simple comparison table showing different components within a lending management system:

| Component | Function Description |

|---|---|

| Loan origination software | Handles application intake and initial approval process |

| Loan processing software | Verifies documents and calculates loan terms |

| Loan servicing software | Manages repayments, interest, and account updates |

| EMI management software | Tracks installment schedules and payment status |

| Credit management system | Evaluates borrower risk and credit history |

| Loan tracking software | Monitors loan lifecycle and borrower activity |

In addition to software tools, educational resources such as financial literacy websites and government portals provide information on loan structures and borrower rights. Templates for repayment schedules and financial planning sheets are also widely used to complement digital systems.

FAQs

What is a loan management system and how does it work?

A loan management system is a digital platform that manages the entire loan lifecycle, including application, approval, disbursement, and repayment tracking. It combines features like loan processing software and loan servicing software to automate and organize these tasks.

What is the difference between loan origination software and loan servicing software?

Loan origination software focuses on the early stages of a loan, such as application and approval. Loan servicing software manages the later stages, including repayment tracking, interest calculations, and account updates.

How does loan tracking software help borrowers?

Loan tracking software allows borrowers to monitor their loan status, view payment history, and check outstanding balances. It improves transparency and helps individuals manage their financial commitments more effectively.

What is EMI management software used for?

EMI management software is used to calculate and track equated monthly installments. It ensures that payment schedules are accurate and helps both lenders and borrowers keep track of due dates and amounts.

Are digital loan platforms safe to use?

Digital loan platforms are designed with security measures such as data encryption and identity verification. They also follow regulatory guidelines, which help ensure that borrower information is handled responsibly.

Conclusion

Loan Management Systems have transformed how lending processes are handled by replacing manual workflows with structured digital solutions. They combine tools like loan origination software, loan servicing software, and credit management systems to manage the full loan lifecycle. These systems improve efficiency, transparency, and compliance while adapting to modern financial needs. As technology continues to evolve, loan automation software and digital loan platforms are expected to become more integrated and user-friendly.